29 May 2026

ACH Transfers Reshape Credit Card Expense Dynamics for Online Subscription Merchants

Online subscription merchants continue to navigate shifting payment landscapes where ACH transfers play an expanding role in managing operational expenses tied to recurring billing, and data released in May 2026 by the Federal Reserve shows ACH volume for consumer subscriptions rose 18 percent year over year. Subscription businesses that once relied almost exclusively on credit card rails now route a growing share of renewals through the Automated Clearing House network because settlement costs sit substantially lower while still delivering reliable collection rates for monthly and annual plans.

Core Mechanics of ACH in Recurring Billing

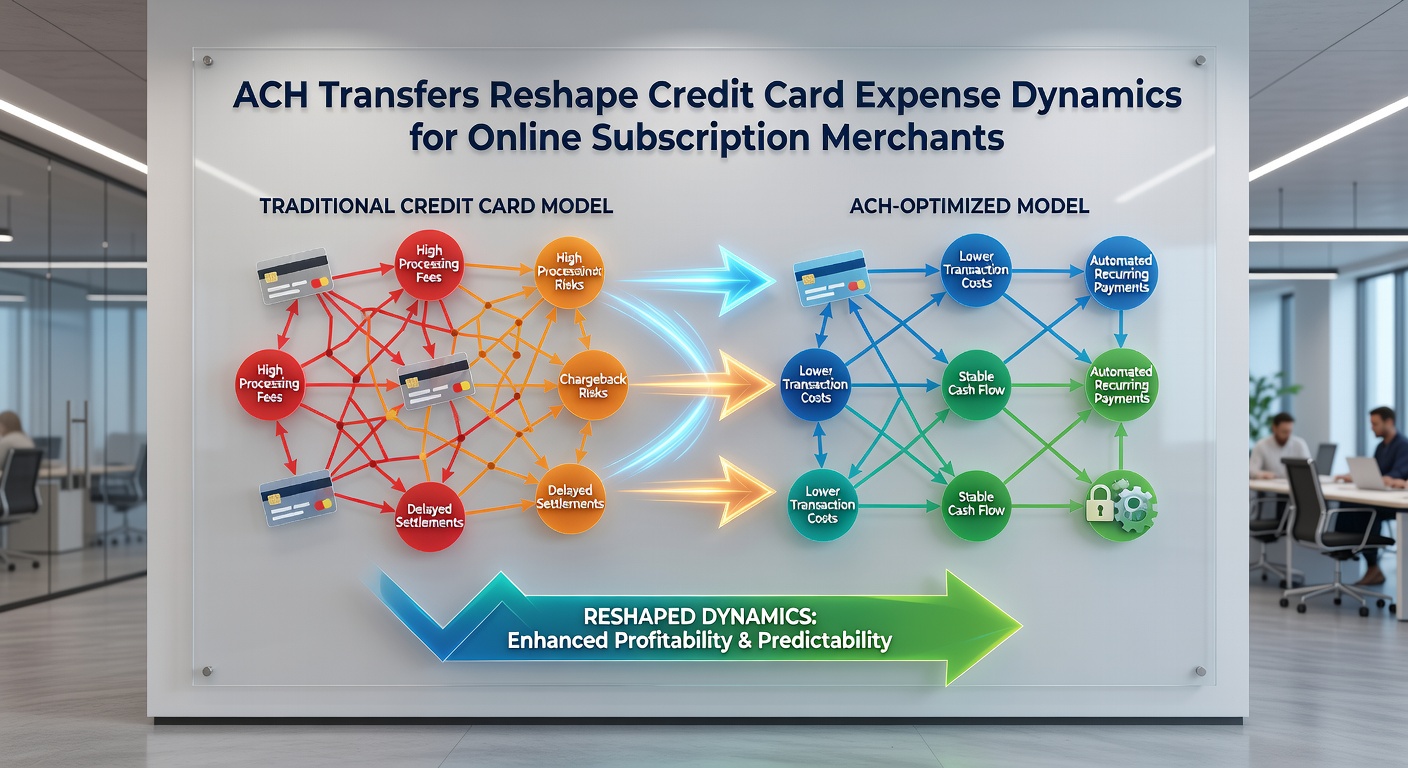

ACH transactions move funds directly between bank accounts through the Federal Reserve's clearing system, bypassing the interchange fees and network assessments that accompany credit card authorizations. Merchants initiate these transfers via their payment processors or banking partners, and the process typically requires customer authorization plus a brief verification window that ranges from one to three business days. Because the underlying infrastructure already exists for payroll and bill-pay services, integration into subscription platforms requires minimal additional development once the gateway connection is established.

Credit Card Cost Structures Under Pressure

Credit card processing carries a mix of fixed and variable expenses that scale with transaction volume, including interchange rates set by card networks, acquirer markups, and PCI compliance overhead. Subscription merchants often face elevated costs when customers store cards for automatic renewals because repeat authorization attempts and occasional declines trigger additional fees. Observers note that average effective rates for subscription merchants hover between 2.5 and 3.5 percent per transaction when all components are tallied, whereas ACH transfers settle at fractions of a cent per dollar in most cases.

Expense Shifts Observed Across Merchant Segments

Smaller subscription services handling fewer than 5,000 active accounts report the most noticeable movement toward ACH because their thinner margins leave little room for percentage-based fees that compound over the customer lifetime. Larger platforms with diversified revenue streams adopt hybrid approaches, offering customers both card and bank transfer options at checkout and then routing the lower-cost method where possible. Research from the Reserve Bank of Australia indicates similar patterns emerging in markets that operate comparable batch settlement systems, with recurring service providers reducing overall payment expenses by 30 to 45 percent after introducing bank transfer alternatives.

Take one SaaS provider that migrated 60 percent of its monthly renewals to ACH over an 18-month period; internal records showed a drop in payment processing spend from 2.9 percent of revenue to 1.4 percent without measurable increases in involuntary churn. The transition also reduced exposure to chargeback disputes, which occur at materially lower rates for bank transfers than for card transactions according to industry settlement reports.

Customer Adoption Patterns and Friction Points

Conversion rates for ACH mandates depend heavily on the onboarding experience merchants provide, and platforms that embed bank verification within the initial signup flow achieve completion rates above 75 percent in multiple case studies. Some customers hesitate because of the multi-day settlement window or concerns about sharing routing details, yet education around fraud protections and the ability to cancel mandates at any time addresses most objections. Processors that support instant account verification through open banking protocols see faster uptake, particularly among users already accustomed to digital banking tools.

Regulatory and Infrastructure Developments Through 2026

Updates to Nacha operating rules that took effect earlier in the decade continue to influence merchant behavior, while new real-time payment rails under development promise to compress settlement times further. In May 2026 the Federal Reserve published updated statistics showing that same-day ACH transactions now account for nearly 22 percent of total volume, a figure that subscription merchants monitor closely because faster funds availability improves cash-flow forecasting. European and Canadian payment frameworks have introduced parallel instant transfer capabilities that subscription platforms in those regions are incorporating into renewal workflows, creating a global convergence around lower-cost account-to-account movement.

Implementation Considerations for Merchants

Integrating ACH requires attention to authorization language, retry logic for failed transfers, and reconciliation processes that differ from card settlement files. Gateways that offer unified reporting across card and ACH channels reduce administrative burden, and several providers now bundle risk-scoring tools that flag accounts likely to experience NSF returns before they occur. Subscription platforms that segment customers by preferred payment method also gain flexibility to apply targeted incentives, such as small discounts for bank transfer sign-ups, without eroding overall margins.

Conclusion

ACH transfers have become a structural component of expense management for online subscription merchants rather than a niche alternative, and the data patterns observed through May 2026 confirm sustained migration away from exclusive reliance on credit card rails. Merchants that map their customer base, optimize onboarding sequences, and align processor capabilities with both card and bank transfer requirements position themselves to capture measurable reductions in payment-related costs while maintaining collection reliability across recurring revenue streams.