3 Jun 2026

How Niche Service Providers Adjust Billing Workflows to Offset Shifting Interchange Variables in Blended Payment Environments

Blended payment environments combine card-present terminal transactions with card-not-present digital submissions, and niche service providers must recalibrate their billing systems when interchange rates shift across card categories and network rules. These providers often handle recurring revenue streams from specialized markets such as professional software subscriptions or equipment leasing, where transaction mixes change daily and fee structures evolve with issuer policies. Data from the Federal Reserve shows interchange costs can vary by several percentage points depending on whether a transaction routes as a premium rewards card or a standard debit entry, forcing workflow updates that segment each payment at the authorization stage.

Mapping Interchange Shifts Within Blended Setups

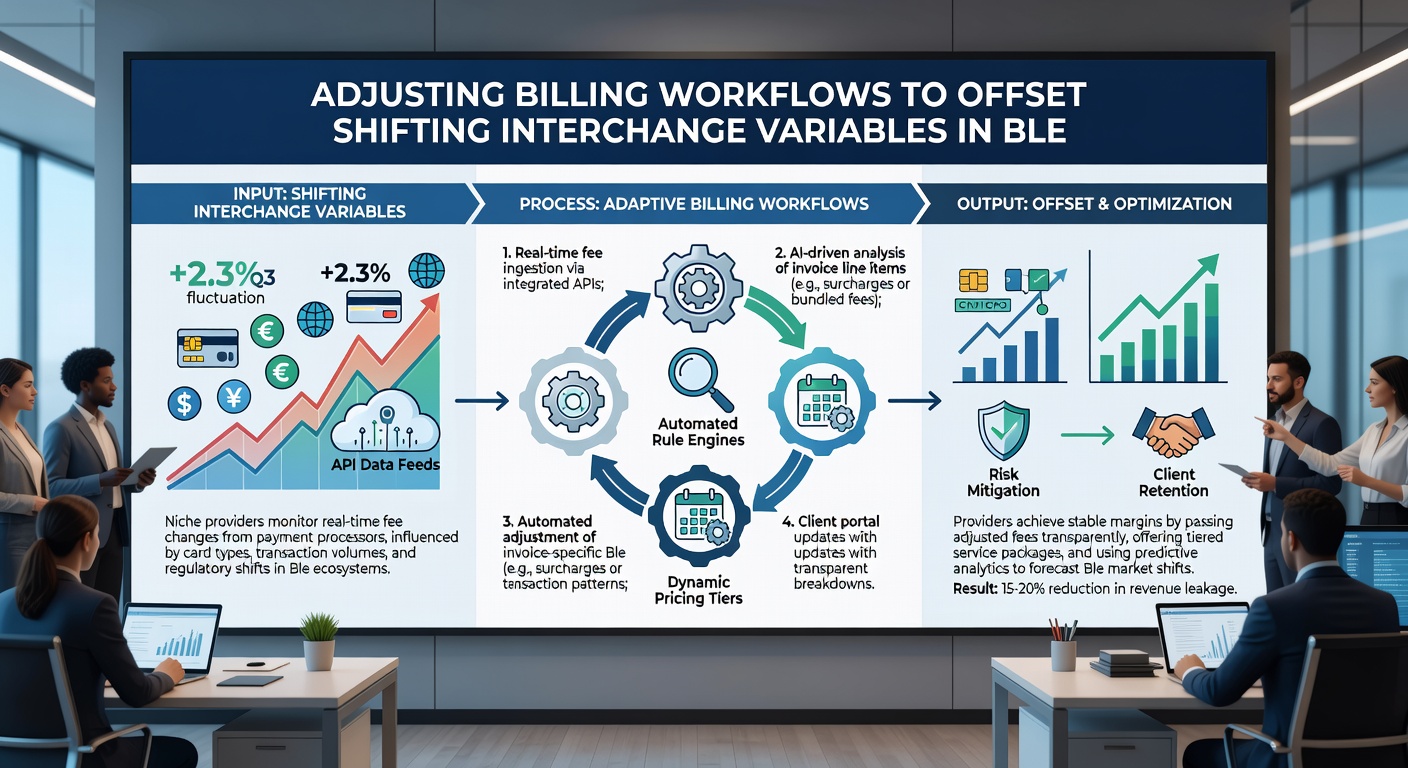

Interchange variables move when card networks adjust qualification criteria, reward program tiers expand, or regional regulations alter how issuers recover costs. Niche providers track these movements through automated categorization engines that classify each incoming transaction by card type, entry mode, and merchant category code before the settlement batch closes. In June 2026 several networks implemented revised rate tables that increased fees on certain e-commerce recurring payments while lowering them on contactless terminal volumes, prompting immediate review of routing logic across hybrid platforms. Observers note that providers who maintain separate ledgers for terminal versus gateway activity gain clearer visibility into which segments absorb the largest cost swings, allowing targeted adjustments rather than blanket price increases.

Reconfiguring Authorization and Settlement Sequences

Service providers revise their authorization sequences so the billing engine evaluates interchange exposure before the payment reaches the acquiring bank. This involves inserting decision trees that compare real-time network tables against historical transaction profiles, then directing premium-card traffic toward processors offering volume-based incentives or alternative funding rails. Those who've studied these patterns find that least-cost routing modules, updated monthly, reduce exposure when blended volumes tilt toward higher-fee categories. Because settlement timing affects qualification, some operators delay batch submission by a few hours to align with updated cutoff windows published by the networks, preserving lower rates without disrupting customer billing cycles.

Dynamic Pricing and Customer Segmentation Tactics

Instead of uniform rate markups, many niche operators embed tiered pricing within their billing software that reflects the interchange profile of each customer's payment method. Subscription platforms, for example, may apply a small differential to accounts that consistently use rewards cards, offsetting the incremental cost while remaining transparent in monthly statements. Research indicates this segmentation maintains margin stability across mixed payment cohorts without triggering widespread customer churn. Workflow engines now pull card-type metadata at signup and store it alongside recurring schedules, enabling automatic repricing when networks reclassify certain BIN ranges mid-cycle.

Integration With Gateway and Terminal Partners

Providers coordinate closely with gateway vendors and terminal manufacturers to receive daily interchange table updates through API feeds rather than manual uploads. This integration allows billing systems to recalculate expected fees for each scheduled renewal before the charge is attempted, flagging outliers for manual review or customer communication. European Central Bank statistics on cross-border card volumes illustrate how blended environments spanning multiple jurisdictions encounter additional layers of variability, leading some operators to maintain parallel rule sets for domestic and international traffic within the same platform. The result is a modular workflow that swaps routing preferences or applies temporary surcharges where permitted by local rules, all while preserving a single customer-facing invoice.

Monitoring, Testing, and Continuous Refinement

Continuous monitoring dashboards compare projected versus actual interchange deductions at the close of each settlement period, highlighting any drift caused by new card issuances or network policy tweaks. Teams run controlled test batches monthly, routing identical transaction sets through alternate processors to quantify savings before committing production traffic. Those who've implemented such testing report faster identification of beneficial routing paths, particularly when blended volumes include both high-value equipment leases and low-value subscription add-ons. Because interchange tables can change with little notice, automated alerts notify finance staff when thresholds are breached, triggering workflow patches that prevent cumulative margin erosion over successive billing cycles.

Conclusion

Niche service providers maintain profitability in blended payment environments by embedding interchange awareness directly into billing workflows rather than treating fees as a static overhead. Through segmented authorization logic, dynamic customer pricing, and tight integration with network data feeds, these operators absorb rate fluctuations without broad service disruptions. As interchange variables continue to evolve, the emphasis remains on modular systems that adapt quickly while preserving accurate, transparent billing for end customers.