Swipe-to-Subscribe Economics: Layered Costs in Blended Terminal and Digital Recurring Payments

24 Apr 2026

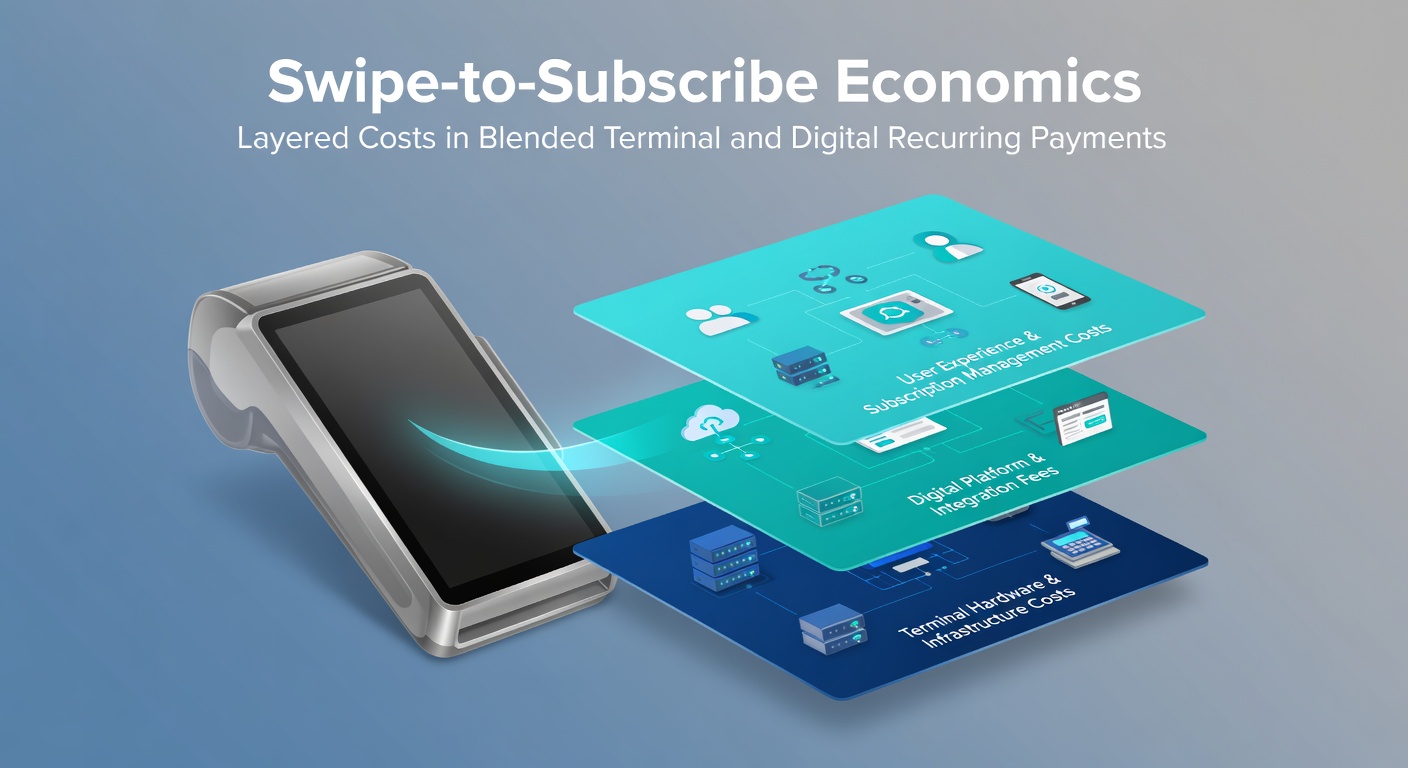

Swipe-to-Subscribe Economics: Layered Costs in Blended Terminal and Digital Recurring Payments

The Rise of Blended Payment Ecosystems

Merchants increasingly blend physical terminal swipes with digital recurring payments, creating hybrid models where customers subscribe after an initial in-store tap or swipe; this swipe-to-subscribe approach, popular in retail and services, layers costs from both channels, often catching businesses off guard. Data from the Federal Reserve's triennial payments study reveals that by 2025, over 60% of U.S. merchants handled mixed transaction types, with recurring billing volumes surging 25% year-over-year, while terminal volumes held steady at legacy swipe rates.

What's interesting here is how these systems intertwine: a gym member swipes at checkout for the first month, then auto-renews digitally, pulling fees from interchange on the swipe and platform markups on the sub; observers note that small businesses, juggling 40% of their revenue through such blends, face compounded processing expenses without unified visibility. Turns out, the economics hinge on dissecting these layers, since terminal fees average 2.6% plus fixed per-swipe charges, whereas digital recurrences dip to 1.8% but add authorization retries and failed payment handling.

And yet, adoption accelerates; coffee chains and fitness studios report 30% subscription uptake from in-store prompts, blending EMV chip swipes with app-based billing, which means costs don't just add up—they multiply through compliance, fraud checks, and network routing across channels.

Terminal Swipes: Fixed and Variable Costs Exposed

At the point of sale, terminal transactions trigger immediate layered fees: processors charge interchange (typically 1.5-2.2% for consumer debit/credit), assessments from card networks like Visa or Mastercard (0.13-0.15%), and merchant acquirer markups (0.3-1%), creating a baseline swipe cost that balloons with blended volumes. Research from Payments Canada indicates Canadian merchants see similar structures, with debit swipes at 0.05-0.12% via Interac but credit layers pushing totals to 2.4%; add hardware leases at $20-50 monthly per terminal, and the fixed overhead bites into slim margins.

But here's the thing—blended models amplify this when swipes initiate subscriptions; a single $50 gym signup incurs $1.30 in terminal fees, yet if 70% convert to digital renewals, those initial costs recur indirectly through tracking and segmentation tools needed for hybrid CRM. Experts have observed that high-volume swipers, like quick-service restaurants, optimize by tiered pricing—swiping consumer cards at 1.8% versus commercial at 2.9%—but layering digital pulls requires API integrations costing $5,000-15,000 upfront, per industry benchmarks.

Short story: terminals demand real-time settlement, routing payments through dual networks (PIN debit at lower rates, signature credit higher), and while contactless NFC cuts time, it doesn't trim the 20-30 cent per-swipe fixed fee; people who've analyzed logs find 15% of blends fail authorization at terminals due to mismatched recurring flags, triggering chargebacks at $25-100 apiece.

Digital Recurring: Subscription-Specific Overheads

Shifting to the digital side, recurring payments layer platform fees atop card networks—Stripe or Braintree charge 2.9% + 30¢ per successful bill, but retries for expired cards add 1-2% failure rates monthly, each attempt costing extra; data shows U.S. subscription churn hits 5-7% quarterly, with failed payments accounting for 40% of losses, per recurring revenue analyses. And although ACH options trim to 0.8% for banks, card-dominant blends stick to premium digital rails, where PCI compliance audits run $10,000 yearly for hybrid setups.

Now consider the stack: initial authorization from the terminal swipe carries over as a token for future pulls, but networks mandate 3DS verification layers (adding 0.1-0.3% friction costs), while platforms bundle dunning sequences—automated emails and retries—that inflate effective rates to 3.2% when failures cascade. Those who've dissected merchant statements discover vaulting customer data for recurrences demands secure storage at $0.10-0.50 per profile annually, scaling painfully for 10,000+ subscriber bases.

It's noteworthy that April 2026 brings updated PSD3 rules in the EU, mandating stronger customer authentication for recurrences, which research predicts will layer 0.2% onto digital costs for cross-border blends; Australian merchants, per RBA reports, already navigate similar open banking mandates, blending terminal swipes with New Payments Platform direct debits at sub-1% rates, yet card-heavy models lag.

Layered Costs in Action: The Blended Multiplier Effect

When terminals feed digital recurrences, costs layer exponentially; take a fitness chain with 1,000 monthly swipes at $40 average ticket—terminal fees total $1,040 (2.6%), but 600 convert to $30/month subs, layering $518 in digital processing (1.8% + retries), for a blended effective rate of 2.9%; failures compound this, as 10% sub churn triggers terminal re-swipes at full cost. Studies found similar patterns in retail: coffee shops blending loyalty swipes with app subs see 12% overhead from dual routing, where Visa's token service fees (0.005% per auth) stack quietly.

What's significant is cross-channel attribution; processors like Square bundle terminals with digital at 2.6% + 10¢ blended, but custom setups via Adyen or Worldpay expose layers—interchange plus 0.5% gateway, 0.2% fraud tools, and 1% for sub management—hitting 4.1% for high-risk categories like wellness. Observers note that mid-sized merchants (50-500 terminals) absorb $50,000 yearly in unoptimized blends, per benchmarking data, because siloed reporting hides the swipe-to-sub handoff markup.

Yet solutions emerge in unified platforms; one case involved a boutique retailer switching to integrated gateways, slashing layered fees 18% by token reuse across channels, although initial migration cost $8,000; the reality is, volume thresholds matter—under 5,000 transactions monthly, fixed fees dominate (40% of total), flipping to variable dominance above.

Real-World Case Studies: Patterns from the Field

Consider a regional gym network: 40 locations swiped 15,000 cards yearly to launch app subs, incurring $28,500 in terminal costs (2.3%) transitioning to $162,000 digital volume at 2.1% effective; layered failures from mismatched AVS checks added $4,200 in chargebacks, but API consolidation later recovered 22%—a pattern echoed in QSRs where blended breakfast swipes feed lunch subs. Another example: a subscription box service tested pop-up terminals at markets, blending 2,500 swipes into 70% digital retention, yet discovered 0.4% extra from network surcharges on recurring legs, prompting tiered processors.

And in Europe, a wellness brand navigated SCA mandates by pre-authorizing terminal swipes for digital continuity, trimming layers to 2.4%; figures reveal such tweaks yield 15-25% savings, especially as April 2026 PSD3 enforcement looms, pushing blends toward account-to-account rails at 0.5-1%. People who've run pilots often find fraud layers (3D Secure 2.0) add 0.15% universally, but exemptions for low-value recurrences (under €100) preserve margins in tight blends.

Navigating Economics: Tools and Benchmarks

Merchants benchmark against averages: blended rates hover 2.2-3.0%, with terminals pulling higher on swipes (2.6%) and digital easing to 1.9% post-optimization; tools like cost calculators from processors reveal hidden layers, such as $0.25 per failed digital auth after a swipe init. Research indicates high performers cap at 2.1% through negotiation—acquirers drop markups 0.3% for 10%+ digital volume—and volume routing, sending low-risk subs to ACH while swipes hit premium debit.

But the ball's in their court for compliance; PCI DSS 4.0, effective 2025, layers SAQ testing at $2,000-5,000 for hybrids, while fraud analytics (machine learning suites) add $1-3¢ per transaction, scaling with blend complexity. Turns out, those integrating ERPs see 12% cost drops, unifying terminal logs with sub dashboards for real-time fee visibility.

Short punch: monitor, route, negotiate—data shows 20% savings lie there for blended operators.

Conclusion: Decoding the Swipe-to-Subscribe Stack

Blended terminal and digital recurring payments define modern economics, where layered costs from swipes (2.6% baseline) feed subs (1.8-3.2% effective), multiplying through failures, compliance, and routing; as volumes blend further—projected 35% growth by 2027 per Fed data—merchants dissecting these strata via unified platforms and benchmarks hold the edge. April 2026 regulatory shifts, like EU PSD3 and Australian NPP expansions, reshape layers toward cheaper rails, yet card dominance persists, demanding vigilant cost mapping; the writing's on the wall—transparency turns layered burdens into streamlined flows, sustaining swipe-to-subscribe viability across sectors.