15 May 2026

Unraveling Expense Layers in Bank Transfer Systems for Automated Renewal Platforms

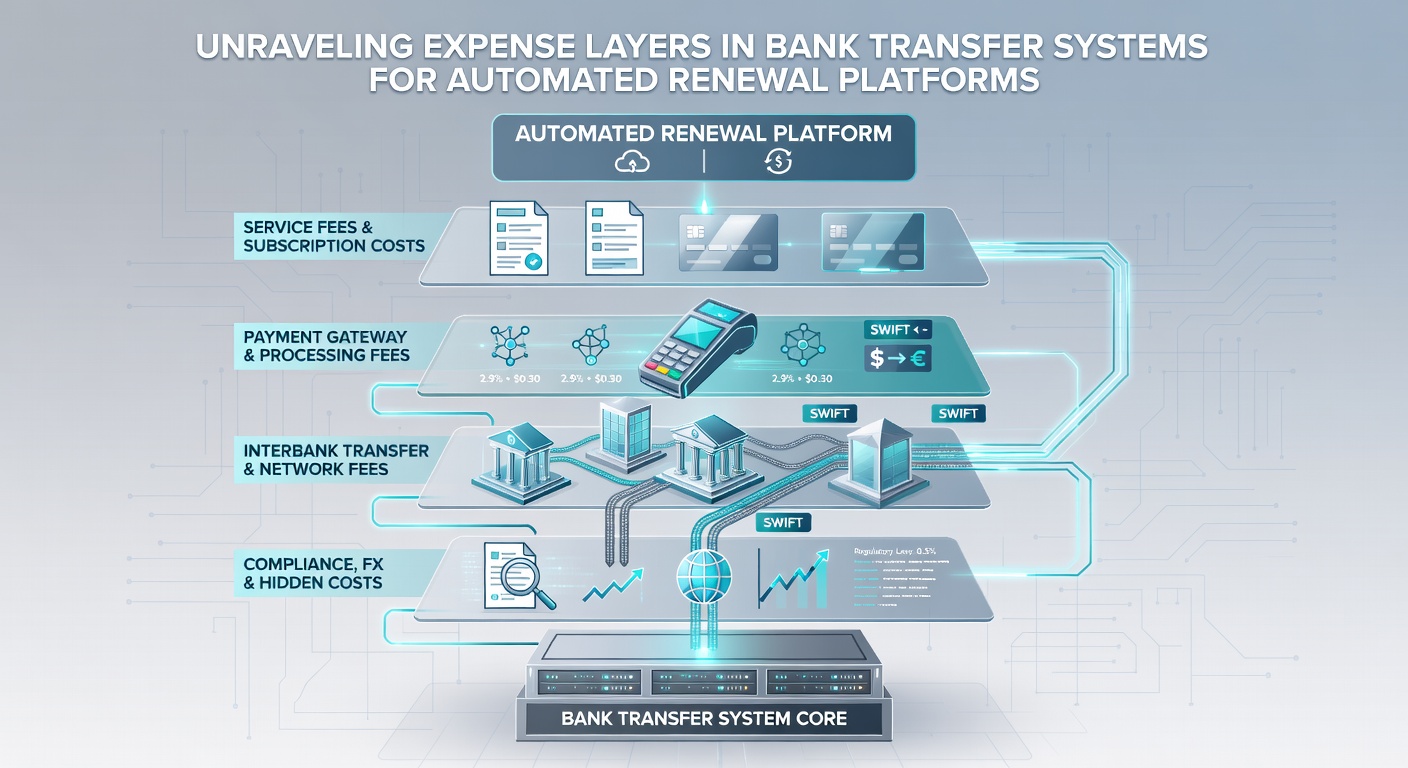

Bank transfer systems form the backbone of many automated renewal platforms that handle recurring payments for subscriptions and services, and these systems carry multiple expense layers that accumulate through origination, processing, and settlement stages. Observers note that each layer adds distinct costs tied to network rules, bank policies, and regulatory compliance, while data from the Federal Reserve shows average ACH transaction volumes reached 7.8 billion in 2024 with continued growth projected into 2026.

Core Components of Bank Transfer Fees

Automated renewal platforms typically initiate bank transfers through ACH networks in the United States or SEPA systems across Europe, and these networks impose per-transaction charges that vary by volume and speed. Originating banks add their own fees for file submission and account verification, while receiving institutions deduct costs for acceptance and return handling. Researchers at the Bank of Canada documented similar structures in domestic systems where settlement finality requires coordination between multiple parties and creates predictable cost stacking for high-volume renewal operations.

Additional layers emerge from compliance requirements such as KYC checks and fraud screening that platforms must complete before each renewal cycle, and these steps often involve third-party service providers who charge per-inquiry rates. International renewals introduce currency conversion spreads and correspondent bank fees that further compound the total expense, whereas domestic transfers avoid some of these variables yet still accumulate network and bank-level charges.

Processing Stages and Their Associated Costs

The first expense layer occurs at initiation when the platform submits a batch file to its originating bank, and this stage includes setup fees plus per-item charges that decrease with higher monthly volumes. The network itself then applies settlement fees based on timing, with same-day processing carrying higher rates than standard next-day options. Experts tracking these flows point out that return rates for insufficient funds or closed accounts trigger additional debit fees at both sending and receiving ends, creating unpredictable spikes for platforms managing large subscriber bases.

During the middle of the process, automated systems perform validation against account databases and fraud tools, and each check adds incremental costs that platforms absorb or pass along depending on their pricing model. By the time funds reach the merchant account, cumulative deductions can represent 0.5 to 2 percent of the transfer amount according to aggregated industry reports, with exact figures depending on contract terms and transaction mix.

Impact on Renewal Platform Operations

Renewal platforms schedule recurring debits weeks or months in advance, and this predictability allows operators to model expense layers more accurately than with card-based systems. Data indicates that platforms processing over 50,000 transfers monthly negotiate lower per-transaction rates at the bank level, yet the network portion remains fixed and creates a floor on total costs. European operators following updated SEPA Instant rules that took effect in prior years now face separate pricing tiers for real-time settlements compared with standard batch processing.

One study of Australian payment patterns revealed that platforms using direct debit for renewals encountered fewer disputes than card transactions, which reduced chargeback-related expenses and offset some of the layered bank fees. Still, integration with core banking APIs requires ongoing maintenance investments that represent a separate operational layer not always visible in per-transaction accounting.

Regulatory and Market Shifts Through 2026

Changes scheduled for May 2026 in certain jurisdictions will adjust disclosure requirements for recurring bank transfers, and these rules aim to increase transparency around cumulative fees for consumers. Platforms must prepare updated consent flows and reporting mechanisms that may introduce new compliance costs during the transition period. Observers following European Central Bank updates note parallel efforts to standardize instant payment pricing across member states, which could compress certain expense layers while elevating others tied to infrastructure upgrades.

Market participants continue to evaluate hybrid models that combine bank transfers with alternative rails to balance cost, speed, and reliability for renewal cycles. Figures from payments research groups show steady adoption of these layered approaches as operators seek to minimize single-point dependencies.

Conclusion

Expense layers in bank transfer systems for automated renewal platforms arise from interconnected fees at origination, network, receiving, and compliance stages, and operators track these components to maintain accurate pricing and margin projections. Data from multiple central banks and industry analyses confirm that volume discounts and timing choices influence the final total, while upcoming regulatory adjustments in 2026 will add further considerations for disclosure and infrastructure. Those managing renewal platforms benefit from mapping each layer against actual transaction patterns to identify opportunities for cost containment without compromising settlement reliability.